Key takeaways

- Economists are assured that the housing market will not be going to crash. As a substitute, it’s present process a correction that can possible take a few years.

- Dwelling costs have continued to climb at the same time as gross sales exercise has slowed, largely as a result of a list scarcity—not a bubble ready to burst.

- Lending requirements are a lot stricter than they have been earlier than the Nice Recession, lowering the chance of a credit-driven collapse.

- Even so, homebuyers and sellers are feeling the pressure of an unaffordable housing market and unstable financial insurance policies.

Right this moment, the housing market feels stuck. Consumers are frozen out by excessive costs and elevated mortgage charges. Sellers are reluctant to record as a result of they don’t need to hand over low-rate mortgages and fear they received’t discover a purchaser. Because of this, gross sales are slow and value cuts are more common. Customers are involved about how dramatically the market has flipped from sizzling to chilly.

However most economists are assured that the economic system is definitely present process a long-term correction, not spiraling uncontrolled. The final actual property crash within the U.S. occurred throughout the Nice Recession almost twenty years in the past, when a housing bubble fueled by dangerous lending triggered a collapse. Right this moment’s market seems to be basically totally different.

So, in case you’re a purchaser or vendor caught on the sidelines questioning if the housing market goes to crash, this text is for you. Let’s break down what a housing market crash seems to be like, why economists are assured we don’t want to fret, and why patrons and sellers are on edge.

From Redfin’s Chief Economist

“We’re in the course of a long-term housing market correction, not a housing market crash. After the pandemic-era frenzy despatched costs hovering and stock to historic lows, the market wanted a reset. What we’re seeing now will not be a sudden collapse however a yearslong comedown: slower gross sales, flatter costs in lots of metros, and patrons getting leverage.” – Daryl Fairweather, Redfin Chief Economist

>> Watch: Home Prices Can’t Crash. Here’s the Math.

What’s a housing market crash?

A housing market crash is a sudden, sharp, widespread drop in house values. Crashes often stem from broader financial or monetary shocks, like a recession, a surge in speculative lending, excessive inflation, or rising unemployment. These pressures can rapidly spill into housing, triggering oversupply or a pointy drop in demand.

Throughout a crash, a number of issues usually occur on the similar time:

- Dwelling costs fall rapidly throughout the nation

- Purchaser demand drops, typically as a result of job losses, excessive rates of interest, or delinquency

- Dwelling gross sales sluggish sharply

- Foreclosures and mortgage defaults improve as householders wrestle to maintain up with funds

Housing crashes not often occur in isolation. They’re often tied to broader financial shifts, resembling recessions, monetary crises, or dangerous lending practices. The final true actual property crash within the U.S. occurred throughout the 2007–2009 Nice Recession, which was linked to a burst housing bubble and mortgage lending disaster.

Why the housing market is unlikely to crash

Whereas the housing market at present is slow, expensive, and impacted by global economic uncertainty, consultants are assured that the housing market will not be going to crash. As a substitute, it’s experiencing a chronic “reset” from the pandemic, when home costs and inflation skyrocketed. In actual fact, exercise lately started moving toward extra regular spring ranges.

“The concept there’s a crash simply across the nook is a story that types at any time when the economic system goes by means of a seismic shift,” mentioned Chen Zhao, Redfin Head of Economics Research. “However at present, indicators are pointing to a comparatively secure reset: Costs are leveling out, mortgage charges are regular, development is rising, and affordability is bettering. However the market continues to be very troublesome, so it’s pure for folks to fret.”

Let’s dive a bit deeper into why economists imagine housing isn’t heading towards a crash.

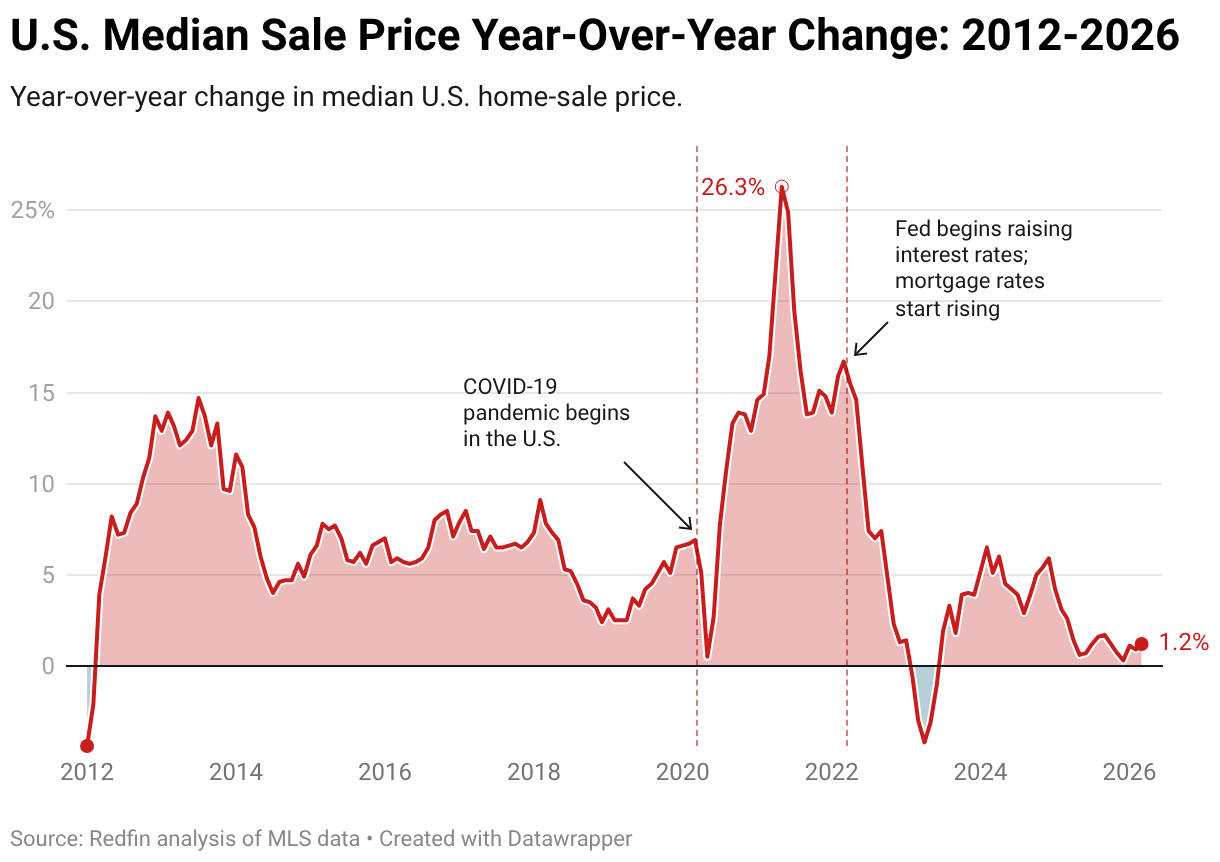

Dwelling costs are rising extra slowly, and can possible stage out

Earlier than a crash, you may see house costs spike sharply after which all of a sudden plunge as a housing bubble bursts. That’s not what we’re seeing at present. Whereas costs are nonetheless rising in lots of markets, the tempo of progress has slowed to round 1%, and most analysts expect costs to flatten in 2026 and past because the market continues to regulate.

After all, there are regional exceptions. Elements of the Midwest and Northeast with comparatively reasonably priced housing and restricted stock are nonetheless seeing value progress. In the meantime, costs are falling in a couple of overheated markets within the Solar Belt, notably Austin, which has flipped from the hottest to the coldest market within the nation.

Mortgage charges are settling into a brand new regular

A sudden improve or lower in mortgage charges can set off main shifts within the housing market, like a surge in demand or sharp drop in listings. That’s not possible to occur at present, barring dramatic motion from the Trump Administration. Whereas charges stay elevated in comparison with pandemic lows, they’ve stabilized relative to the fast will increase seen in 2022 and 2023.

“It’s unclear precisely what would occur if charges dropped dramatically—however we most likely wouldn’t see a surge in costs,” continued Zhao. “One motive is as a result of a drop in charges would possible imply the economic system is in a recession, which might restrict patrons’ spending energy. One other is as a result of extra provide may hit the market as sellers develop into “unlocked” from their pandemic-era charges. That is already starting to occur: The share of householders with mortgage charges above 6% now outnumbers these with charges beneath 3%, which is resulting in a sluggish improve in stock.”

The labor market is comparatively robust

Unemployment and job progress have an outsized affect on the housing market. Mass layoffs and rising unemployment are two of the principle triggers of housing crashes, as a result of they will result in missed mortgage funds, pressured gross sales, and rising foreclosures. When lots of people rapidly lose their revenue, housing demand typically drops—and provide spikes as financially strained householders are pressured to promote.

That’s not what we’re seeing at present.

“The job market has been holding up comparatively nicely, which is why we aren’t seeing a surge in foreclosures or delinquencies,” added Zhao. “There are some worrying alerts that employment might shift sooner or later—particularly surrounding the rise of synthetic intelligence (AI), and job progress that has nearly exclusively been concentrated in healthcare. However secure employment is a key motive economists don’t anticipate a wave of foreclosures or distressed gross sales.”

There are stricter lending necessities

Laws put in place after the 2007-2009 monetary disaster tightened mortgage lending requirements to scale back dangerous loans and stop one other broad mortgage-credit collapse. These guidelines—like requiring banks to carry extra money in reserve to cowl potential lending losses—make it much less possible that credit score alone will ignite one other crash.

“We’re unlikely to see one other credit-induced financial collapse given the strict lending requirements set in 2010 and strengthened in 2024,” famous Fairweather. “Stronger oversight and extra clear underwriting makes the housing market much more resilient than it was twenty years in the past. The Trump administration has recently proposed easing a few of the Recession-era guardrails to get banks again into the mortgage enterprise, however it’s unclear what impact this may have.”

Why patrons and sellers are anxious a couple of housing market crash

Regardless that an actual property crash is unlikely, on a regular basis Individuals are nonetheless coping with the results of a unstable and really unaffordable housing market—especially youthful generations.

To higher perceive the difficulties, let’s break down some key information behind at present’s market.

The pandemic housing growth and bust

The pandemic threw the housing market off kilter and gave patrons and sellers a serious case of whiplash, which prompted some experts to worry {that a} crash was potential.

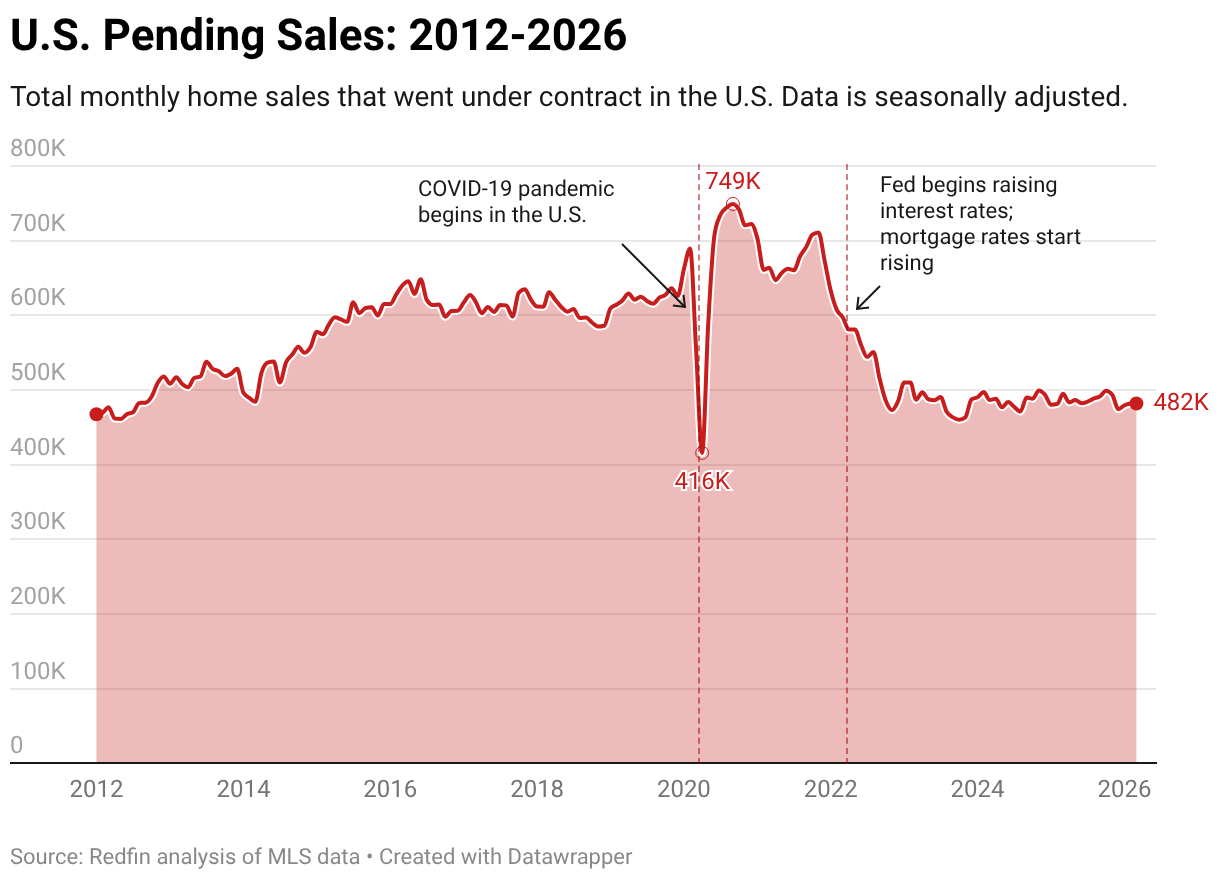

Actual property exercise grinded to a halt in early 2020 earlier than skyrocketing to record heights in 2021-2022, as distant work and ultra-low mortgage charges unleashed a shopping for frenzy centered within the Solar Belt. However when mortgage charges spiked and affordability collapsed in 2022–2023 as a result of historic inflation, demand fell sharply.

Right this moment, the housing market is within the early levels of restoration, with many patrons nonetheless priced out and sellers ready for exercise to return. Worth cuts are fairly common nationwide and common within the Solar Belt the place most individuals moved throughout the pandemic—particularly Austin, Nashville, and San Antonio.

There are nonetheless some outlier cities clustered within the Midwest and Northeast the place properties are promoting like sizzling muffins and costs are rising, like Buffalo and Milwaukee. However that’s largely as a result of they’re extra reasonably priced and have a smaller pool of properties for patrons to select from.

A possible “housing bubble”

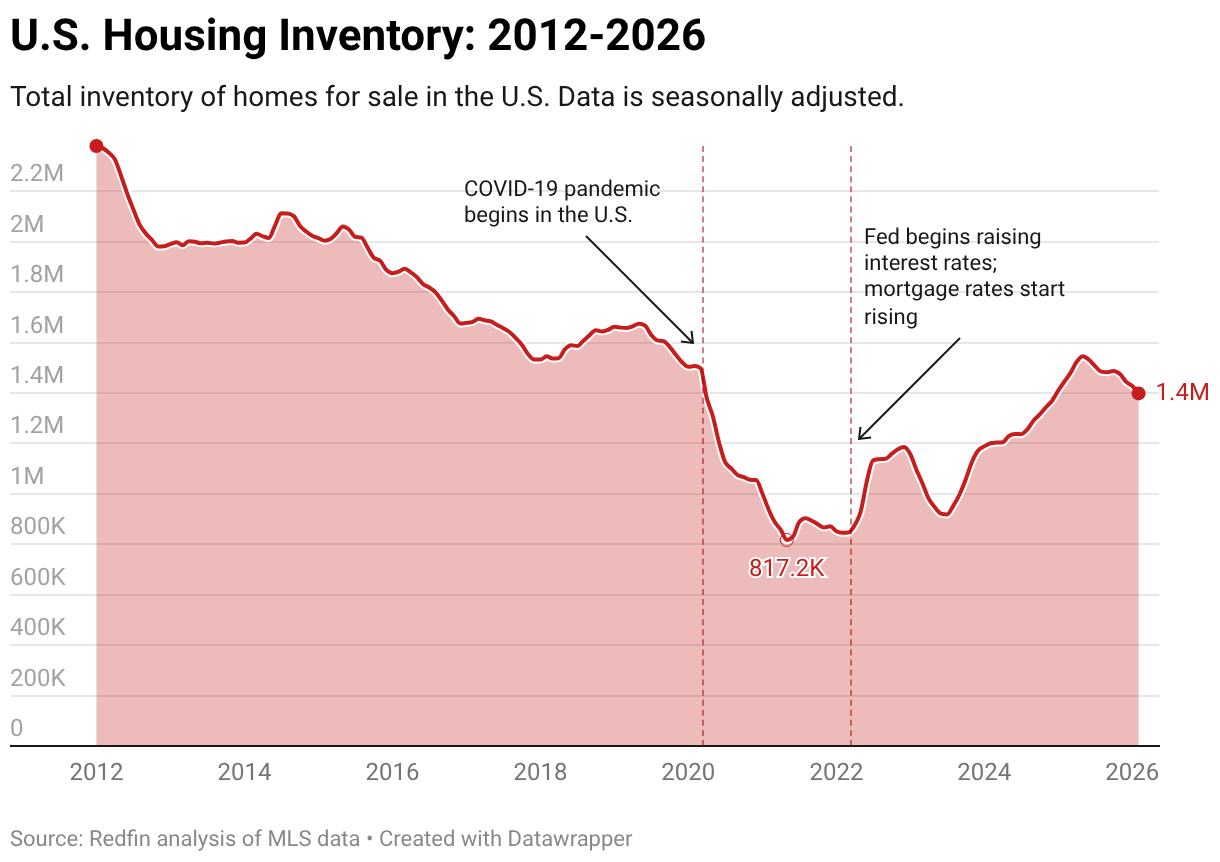

Dwelling costs have hit new month-to-month information for greater than two years in a row, raising concerns about whether or not actual property is in “bubble” territory—when costs are unsustainably inflated. Plus, though value progress has slowed from the breakneck tempo of the pandemic, costs themselves are still rising and stay close to file highs in lots of elements of the nation. A serious stock scarcity is basically responsible—which is steadily bettering.

Nevertheless, a couple of consultants have noted that the bigger drawback could also be a scarcity of reasonably priced properties. Those that can afford a house at present are sometimes nonetheless shopping for, however most shoppers are merely priced out.

Report-low affordability and financial unease

Perhaps most significantly, Individuals reside by means of a chronic interval of uncertainty and record-low affordability. Elevated mortgage charges, stubbornly excessive house costs, and broad financial nervousness have made housing really feel out of attain for many individuals.

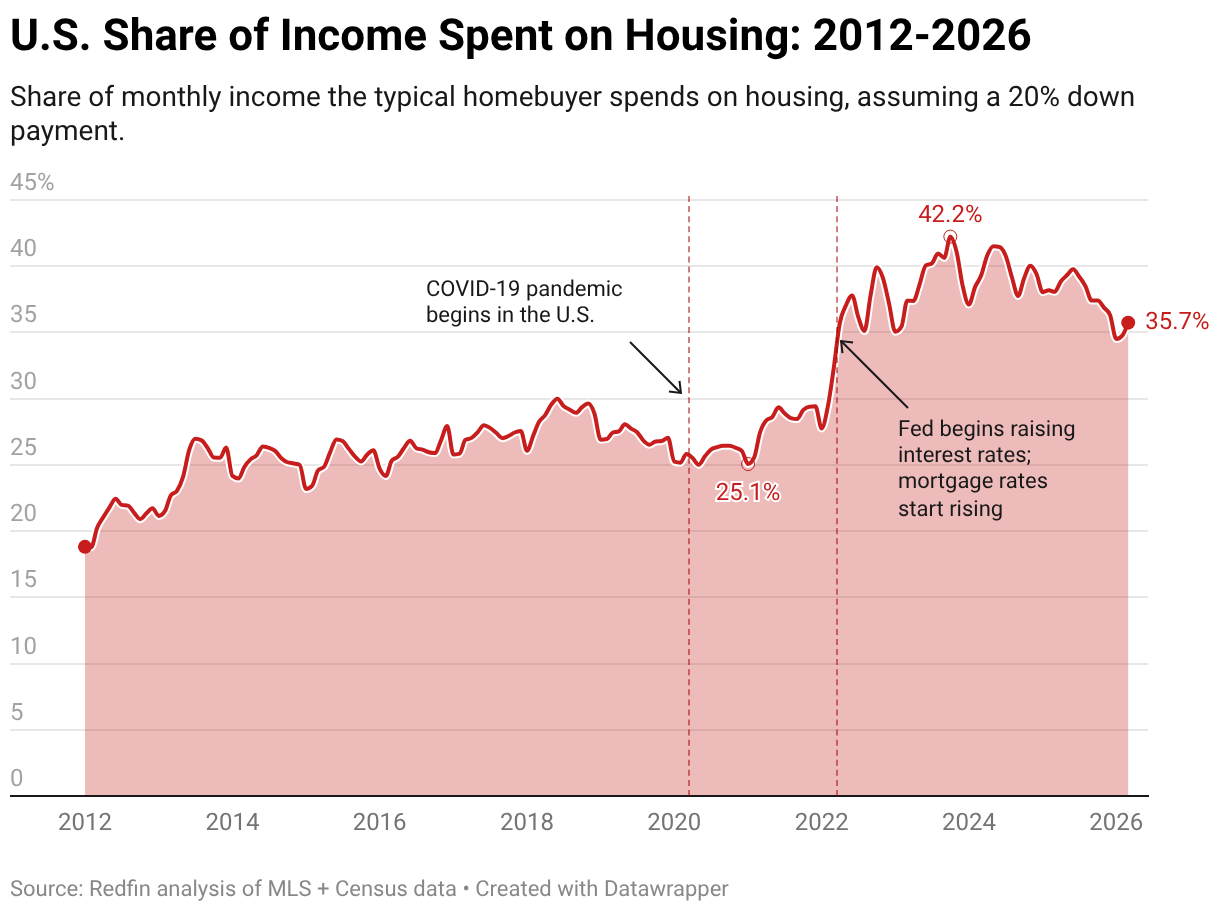

In response to Redfin data, the everyday homebuyer spends about 36% of their revenue on housing (as of March 2026), whereas house costs have risen roughly 40% for the reason that pandemic.

However affordability ought to to enhance as value progress slows and wages rise. And it’s potential that costs will return to “normal” by 2030, which means a median earner will have the ability to afford a median-priced home spending 30% of their revenue on month-to-month funds.

Even so, the combo of monetary stress and uncertainty is reshaping how patrons and sellers behave. It’s one of many largest causes the market feels so unstable, even with out the indicators of a bubble bursting.

Is business actual property crashing?

In contrast to the residential actual property business, business actual property (CRE) has been grappling with a prolonged downturn that started in March 2020. It’s not essentially crashing, however it’s struggling.

When the pandemic hit, most in-person exercise shut down nearly in a single day. This led to a sudden soar in distant work, a web-based purchasing growth, and a change in spending habits as a result of inflation. These modifications, plus spiking rates of interest, weighed closely on workplace buildings and large field shops and dramatically lowered demand for business actual property. Traits have persevered, pushing workplace mortgage delinquencies to record highs—at the same time as distant work fades.

Including one other layer of uncertainty, the fast rise of synthetic intelligence (AI) is beginning to shape investor sentiment within the sector. Some buyers are more and more cautious of industries seen as extra uncovered to AI-driven workforce modifications—notably, entry-level white-collar roles at tech firms that lease or personal business actual property.

“Business actual property has been caught within the crossfire of a number of main financial shifts, and it’s feeling the results,” continued Fairweather. “To adapt, some firms and cities have tried to seek out modern methods to convert vacant workplace buildings into residential buildings, which is constructive on paper. However zoning restrictions and the price of conversion have prevented this from turning into widespread. If present traits proceed, it’ll take fairly some time for the business to get well.”

It’s value noting that the CRE downturn is nowhere close to as robust because the Nice Recession or prolonged valuation pressures of the Nineteen Eighties and early Nineties. Right this moment, stress is extra concentrated in particular property varieties and tied to structural shifts in work and rates of interest fairly than a broad monetary disaster.

The underside line: The housing market is present process a correction, however it’s not crashing

The housing market is most certainly not heading towards a crash. As a substitute, it’s present process a long-term correction. A housing market correction is a slower, typically uneven normalization in costs, stock, demand, and different financial components.

Right this moment, costs are flat or falling in lots of overheated markets, gross sales are slower, stock is constructing, and buyers have more negotiating power. There isn’t the wave of foreclosures, plummeting house values, or systemic monetary stress that defines a crash. For some patrons who can afford to buy now, at present’s market could supply extra alternatives than the extremely aggressive circumstances of the early 2020s.

It’s arduous to say what the longer term will appear like. But when present housing traits proceed, the housing market will develop into extra accessible for extra folks within the not-too-distant future.

Source link