Tokenization doesn’t robotically make hard-to-trade property liquid, business executives stated at Paris Blockchain Week, pushing again on the concept that placing personal credit score, actual property or different illiquid merchandise onchain will by itself create lively secondary markets.

Talking throughout a panel moderated by Cointelegraph CEO Yana Prikhodchenko, Oya Celiktemur, Ondo Finance gross sales director for Europe, the Center East and Africa (EMEA), said there may be nonetheless a false impression that tokenizing illiquid property could make them simpler to commerce.

“I feel there’s nonetheless this concept that tokenizing one thing illiquid will someway magically make it a liquid asset, which is simply not true,” stated Celiktemur. She added that property like actual property and personal credit score “had been by no means that liquid” to start with.

Francesco Ranieri Fabracci, head of tokenization enlargement at Tether, made an identical level. “It’s not that for those who put an asset onchain, it is going to be liquid,” he stated, arguing that solely a narrower set of devices, together with bonds, cash market funds and stablecoins, are more likely to obtain constant liquidity in tokenized markets.

The dialogue comes because the tokenized real-world asset (RWA) sector continues to expandshifting consideration from issuance progress towards whether or not tokenized merchandise can obtain significant exercise and transfer past restricted distribution channels.

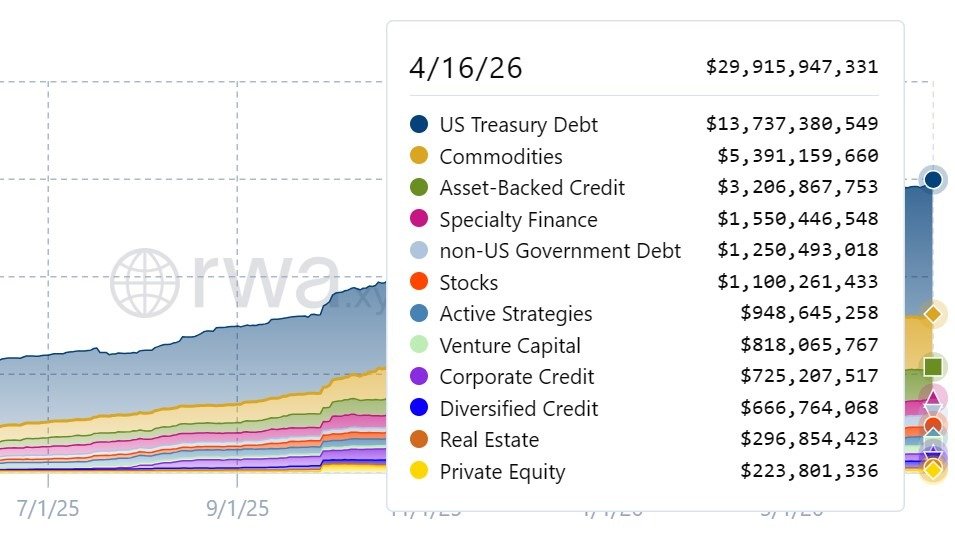

Tokenized RWA market grows, however stays concentrated

Information from RWA anayltics platform RWA.xyz exhibits the tokenized RWA market expanded from $8.8 billion on April 16, 2025, to roughly $29.9 billion on April 16, 2026, greater than tripling in dimension in a single 12 months.

The expansion was led by comparatively standardized and broadly traded property. Tokenized US Treasury Debt and commodities accounted for a big share of the market all year long.

Associated: French minister says new measures are coming after crypto kidnappings

Against this, classes usually related to decrease liquidity remained comparatively smaller regardless of robust proportion progress. Tokenized actual property elevated from about $35 million to $296 million, whereas personal fairness rose from practically $60 million to $223 million.

Different segments, together with asset-backed credit score and company credit score, additionally expanded sharply in absolute phrases, indicating rising issuance throughout a broader vary of devices.

However market worth alone doesn’t show liquidity. Excellent worth can rise as a result of extra property are issued, even when secondary market buying and selling stays skinny.

Journal: Singapore isn’t a ‘crypto hub’ — it’s something better: StraitsX CEO

Source link