With a market cap of $234.6 billion, Wells Fargo & Firm (WFC) is likely one of the largest monetary providers corporations in the US. The corporate offers a variety of banking, funding, mortgage, and shopper and industrial finance services each domestically and internationally.

Corporations valued at $200 billion or extra are usually thought-about “mega-cap” shares, and Wells Fargo suits this criterion completely. It operates via 4 principal segments: Shopper Banking and Lending; Business Banking; Company and Funding Banking; and Wealth and Funding Administration.

Extra Information from Barchart

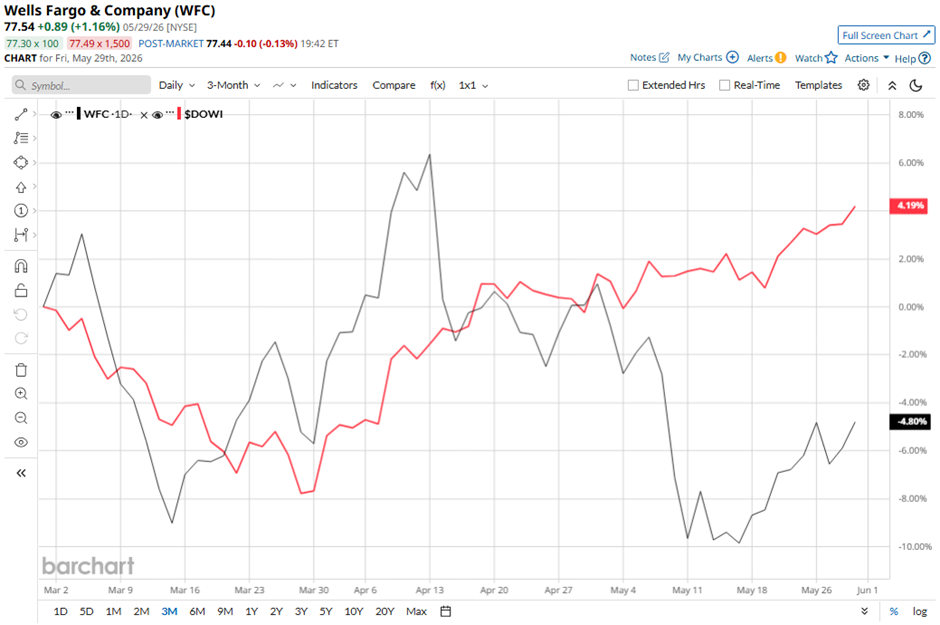

The San Francisco, California-based firm inventory has declined 20.7% from its 52-week excessive of $97.76. Shares of Wells Fargo have declined 4.8% over the previous three months, lagging behind the Dow Jones Industrials Common’s ($DOWI) 4.2% acquire over the identical time-frame.

WFC inventory is down 16.8% on a YTD foundation, underperforming DOWI’s 6.2% return. As well as, shares of the most important U.S. mortgage lender have risen 5.2% over the previous 52 weeks, in comparison with Dow Jones’ 21.2% enhance over the identical time-frame.

The inventory has been buying and selling under its 50-day shifting common since January. Additionally, it has fallen under its 200-day shifting common since early February.

Shares of Wells Fargo fell 5.7% on Apr. 14 regardless of a slight EPS beat as a result of traders targeted on weaker-than-expected income and internet curiosity revenue (NII). Whereas Q1 2026 EPS of $1.60 exceeded estimates, income of $21.45 billion and NII got here in at $12.10 billion, each missed consensus. Investor issues had been compounded by a 21.8% year-over-year enhance in provision for credit score losses to $1.14 billion, a decline within the CET1 capital ratio to 10.3%, and the corporate merely reaffirming its 2026 NII steerage of roughly $50 billion, under the consensus forecast.

Moreover, WFC inventory has underperformed its rival, Citigroup Inc. (C). Citigroup inventory has soared 7.9% on a YTD foundation and 67.8% over the previous 52 weeks.

Regardless of Wells Fargo’s underperformance, analysts stay reasonably optimistic about its prospects. The inventory has a consensus score of “Reasonable Purchase” from 25 analysts’ protection, and the imply worth goal of $97.81 is a premium of 26.1% to present ranges.

On the date of publication, Sohini Mondal didn’t have (both instantly or not directly) positions in any of the securities talked about on this article. All info and information on this article is solely for informational functions. This text was initially printed on Barchart.com