Bonds are imagined to be the boring a part of a portfolio.

They pay revenue, dampen volatility, and assist offset inventory market ache when buyers run for security.

However Morgan Stanley cracked open 150 years’ worth of stock and bond data and located the catch. When inflation runs sizzling, bonds have traditionally turn out to be much less dependable as a inventory market shock absorber — and inflation continues to be operating sizzling sufficient to maintain that danger alive.

A traditional 60/40 portfolio — 60% shares, 40% bonds — is constructed on a easy concept. Shares drive long-term development. Bonds present stability when the trip will get tough.

That playbook broke down after the inventory market peaked on the finish of 2021.

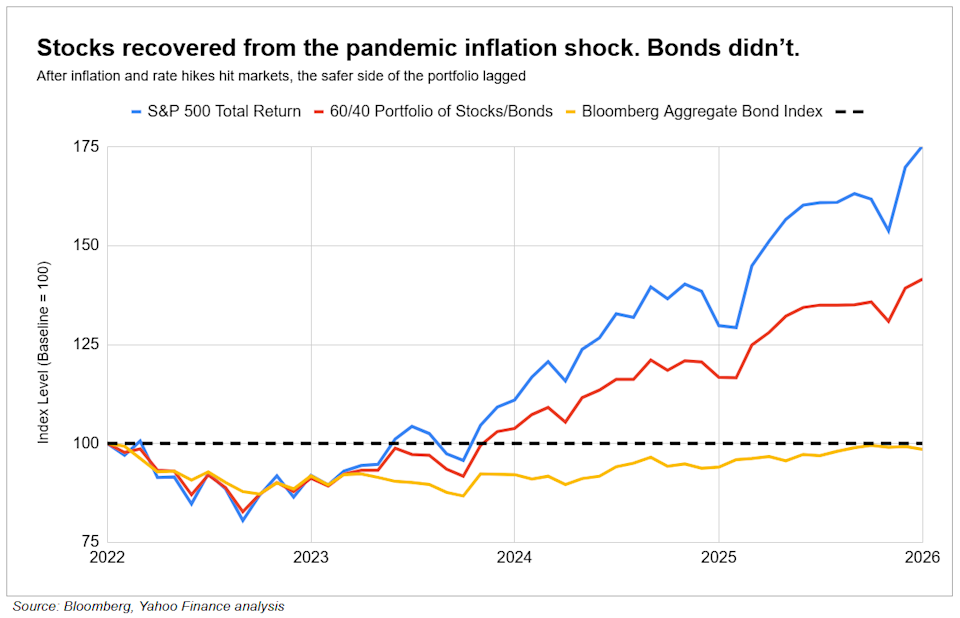

The S&P 500 complete return index — the blue line within the chart — has surged nicely above its early-2022 stage. A 60/40 portfolio — in crimson — has additionally climbed again above that start line, however with a lot much less pressure. In the meantime, the Bloomberg Combination Bond Index — in yellow, a broad measure of high-quality US bonds — has solely clawed again to roughly the place it started the interval.

That really flatters bonds a bit. The bond index had already peaked earlier than the chart begins and nonetheless has not absolutely recovered.

The ache has been even clearer in long-term bond funds just like the iShares 20+ Yr Treasury Bond ETF (TLT), which has been pushed again towards pre-financial-crisis prices.

Inflation broke the previous playbook

When inflation jumped, the Federal Reserve raised rates of interest aggressively. Larger yields helped make bonds extra enticing for revenue, however in addition they hammered bond costs.

That’s the primary bond math. When yields rise, older bonds with lower payouts become less attractiveso their costs fall.

The identical greater yields additionally pressured shares by making future income value much less in as we speak’s {dollars} and tightening monetary circumstances throughout markets. In 2022, shares and bonds fell collectively as an alternative of offsetting one another. Shares later recovered far more rapidly, however the bond aspect by no means delivered the identical rebound.

Morgan Stanley discovered the inflation change

The agency discovered that inflation has traditionally been the most important driver of how shares and bonds transfer collectively. The market time period is correlationwhich merely means two investments are likely to rise and fall collectively or transfer in reverse instructions.

For balanced buyers, adverse correlation is most useful. Shares fall, bonds rise, and the portfolio will get a cushion. Optimistic correlation is the issue. Shares fall, bonds fall, and the cushion will get thinner — or worse, turns right into a drag.

Morgan Stanley discovered that when inflation moved above 2.4%, shares and bonds tended to maneuver extra in the identical route. That’s the line buyers ought to care about now.